The tremors from Strategy’s Q1 earnings call are still rippling through the crypto and equity markets. Executive Chairman Michael Saylor, a figure synonymous with Bitcoin’s corporate adoption, floated the idea that the company might dip into its 818,334 Bitcoin reserves to pay dividends. This isn’t just idle chatter; the implications for a company that has use its balance sheet to become the world’s largest publicly traded corporate Bitcoin holder are profound.

It’s a bold, perhaps even desperate, pivot. Strategy, formerly MicroStrategy, reported a colossal $12.54 billion net loss for Q4, a figure that dwarfs its operational revenue and even its considerable Bitcoin holdings. Yet, it’s these very holdings, acquired at an average cost of $75,537 per coin, that Saylor now suggests could be monetized to meet financial obligations. The plan: use credit to buy Bitcoin, let it appreciate, and then sell pieces of it to cover the bills – in this case, approximately $1.5 billion in annual dividend and interest payments.

The Arithmetic of Appreciation and Obligation

Here’s the stark reality: Strategy has about 18 months of dividend coverage based on its current USD reserves. That’s not a long runway for a company that seems determined to maintain a dividend payout while simultaneously holding an asset known for its volatility. Saylor’s strategy hinges on continuous appreciation of Bitcoin, a bet that the digital gold will outperform not just inflation, but also the interest rate costs of the debt used to acquire it, and the dividend yield.

“We will probably sell some bitcoin to pay a dividend just to inoculate the market and send the message that we did it.”

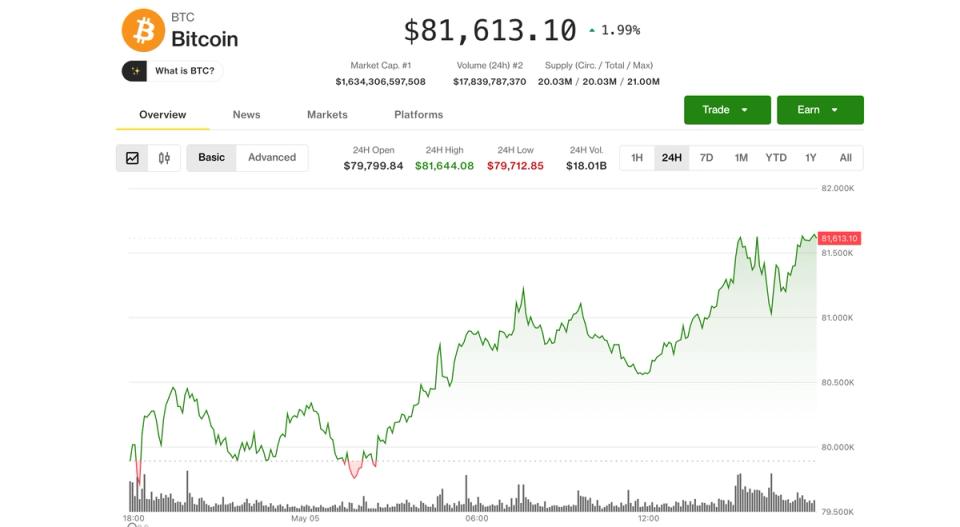

That quote, delivered with a certain bravado, reveals a dual objective: funding obligations and telegraphing confidence. But is it genuine confidence, or a carefully constructed narrative to mask underlying financial pressures? The market’s immediate reaction — a 3% drop in the stock after hours and Bitcoin dipping below $81,000 — suggests a healthy dose of skepticism.

Is This a Sustainable Model for Bitcoin Holders?

Saylor has built Strategy into a high-octane Bitcoin proxy. His thesis has always been that Bitcoin’s potential for appreciation far outstrips traditional asset returns, and that by using use, he can magnify those gains. For a while, it worked spectacularly. But the current economic climate, with higher interest rates and a more uncertain geopolitical landscape, adds new layers of risk to this high-use, single-asset bet.

The $12.54 billion Q4 loss, while attributed in part to accounting rules regarding digital assets (specifically, unrealized losses), doesn’t paint a picture of strong underlying profitability. It highlights the speculative nature of holding such a volatile asset on the corporate balance sheet, especially when debt is involved. Selling Bitcoin to pay dividends feels less like a strategic innovation and more like a necessary response to immediate financial pressures.

This move, if executed, would set a precedent. Corporate entities that have amassed significant Bitcoin holdings might now feel compelled to explore similar avenues to satisfy shareholder demands for income, even if it means selling the very asset intended for long-term appreciation. It could commoditize Bitcoin in a way that many proponents find unpalatable.

Bitcoin’s Volatility Meets Corporate Finance

Think about it: we’ve seen companies borrow against their Bitcoin. We’ve seen them use Bitcoin as collateral. Now, we’re talking about them selling Bitcoin to pay dividends. This is a material shift. It suggests that Bitcoin is no longer just a digital treasure chest; it’s becoming an operational asset in the corporate finance playbook, with all the attendant pressures of traditional finance.

The irony is that Saylor has long championed Bitcoin as a hedge against inflation and a store of value, a digital alternative to gold. Yet, now he’s proposing to sell it to meet regular dividend obligations, much like a company might sell off inventory or a division to cover payroll. It’s a practical, almost mundane, application of a supposedly revolutionary asset.

My take? This is less a strategic masterstroke and more a pragmatic, if slightly alarming, maneuver to maintain the appearance of financial stability and shareholder returns. The market is rightly questioning the long-term viability of a model that relies on the continuous appreciation of a highly volatile asset to fund predictable outflows.

What’s Next for Strategy and Its Bitcoin?

Strategy’s ~818,334 BTC represents a significant portion of the global circulating supply. Any substantial sale by the company could indeed create ripples. The strategy of “buy with credit, appreciate, sell to pay dividends” sounds elegant on paper, but in practice, it’s a tightrope walk. One wrong step—a prolonged crypto winter, a sudden spike in interest rates, or an unexpected corporate event—and the entire edifice could crumble.

This situation underscores the fundamental challenge of integrating volatile digital assets into traditional corporate finance structures. While Saylor might intend to “inoculate the market,